Interview with Uma Rajah, CEO at CapitalRise

"CapitalRise is a specialist lender focusing on prime institutional grade real estate. We put a lot of attention into each loan we underwrite and really engage with the borrower. The most important thing for a lender is the quality and the performance of your loan book, which will ultimately be defined by the quality of your underwriting team.

Quality underpins everything we do. The quality of prime institutional grade real estate we lend against and the quality of the team sourcing and underwriting these opportunities help to ensure the quality and performance of our loan book."

CapitalRise is a specialist property finance crowdfunding platform, focused on high-quality residential & commercial property projects in the UK.

Today we talk with Uma Rajah, co-founder and CEO of CapitalRise, about her real estate vision and expertise and CapitalRise’s approach to high quality lending:

When Alex Michelin and Andrew Dunn decided to found CapitalRise and you joined them as co-founder, how was the process of starting the project and why did you decide to create the company?

In 2016, I was headhunted to join my co-founders at CapitalRise, to take their business idea and build the proprietary tech required to make it a reality.

Alex and Andrew both have strong backgrounds in prime property development - and having founded luxury real estate development business Finchatton nearly 20 years ago, they have since delivered over £1.5 billion worth of luxury real estate, with another billion currently under construction.

Throughout their career as prime property developers, the single most painful part of their business has been sourcing finance for projects.

In the UK, many traditional lenders retreated from the prime property finance market as a result of regulatory changes following the global financial crisis. This left a big gap in the market, which a lot of alternative lenders like CapitalRise are now working to fill.

Alex and Andrew also experienced first-hand the poor and sluggish service property developers receive from traditional lenders - it can take months of painful bureaucracy and a lot of paperwork to get a loan. This really highlighted the opportunity in the market, to provide fast, cost effective and bespoke finance to prime property developers, with expert service from a team of market specialists.

All that was required to complete their team was FinTech expertise and when they approached me to join them, I could see the market opportunity was massive, and jumped at the chance to be part of this exciting venture.

What is the approach or vision of CapitalRise?

CapitalRise’s vision is to disrupt and democratise the prime property finance and investment market. We have two main customer bases - one side of the business, we provide specialist, flexible finance for prime property developers across prime central London and the Home Counties.

On the other, we offer a range of investors, from institutional to retail, access to the finest quality of real estate development investments.

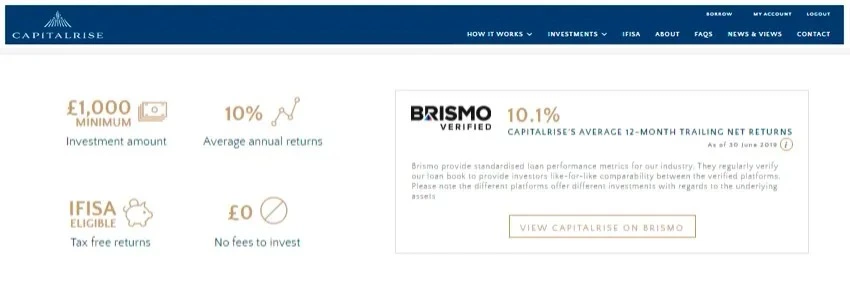

Historically, only institutions and ultra-high net worth individuals, with minimum ticket sizes of a million pounds or more would ever have had access to this part of the private debt investment market. Our vision in building the platform was to bring these institutional grade opportunities to smaller investors, with a minimum investment amount of just £1,000.

Even today, three years after we launched CapitalRise, there are still no other platforms out there offering investors access to invest in the development of such high quality of real estate.

What are the figures for CapitalRise? What is the average yield you are offering? Number of investors, average ticket, number of projects financed, etc.

We're growing very fast. Our investor numbers have increased 238% over the last 12 months and over the same period our lending volumes have increased 5x versus the preceding 12 months. Further to this, we have now lent almost £50m against property assets worth over £315m, with over £30m lent in 2019 to date.

On the investor side, our opportunities offer investors potential returns of between 8-12% per annum and we've so far redeemed £16.1 million to investors with an average return of over 10% p.a.

Whilst we primarily target high net worth and sophisticated investors, investment size ranges from £1,000 all the way up to £300,000 into individual loans across a broad spectrum of investors, from all different of walks of life and age groups. Overall, it seems to be a product that has a very broad appeal.

Could you tell us in more detail what the investment process with CapitalRise is like?

Our entire investment process, from registration to investment, is digital. We complete KYC and AML checks automatically for UK customers, and for overseas customers if we can't identify you automatically, then we might request some further documentation.

UK investors can choose to use their annual £20,000 ISA allowance to invest and earn returns tax-free via our Innovative Finance ISA (IFISA). We were one of the first platforms to start offering the IFISA product when it was launched and we’ve seen great uptake, with over 50% of our customers now opening an IFISA to invest with us.

All opportunities are pre-funded by CapitalRise before being offered as investment opportunities, so as soon as investor funds are received, they are assigned to the selected project and start accruing a return straight away.

We don’t charge investors to invest, instead we generate our revenue from our borrowers, charging them an arrangement fee for arranging the loan and an exit fee when the loan exits. We also take a margin on the interest, which varies but can be up to 2%.

All CapitalRise loans are actively monitored, so investors receive regular updates on how the projects they have invested in are progressing.

An investment redemption will typically happen as a result of the finished property being sold or refinanced. Most of our opportunities pay out at the end of the loan term and to date all repayments have been on time and on business plan, delivering investors an average of 10% p.a. since inception.

Last year CapitalRise won the Newcomer of the Year award, at the RESI Awards, organized by Property Week. What is the novelty you have brought to the lending market?

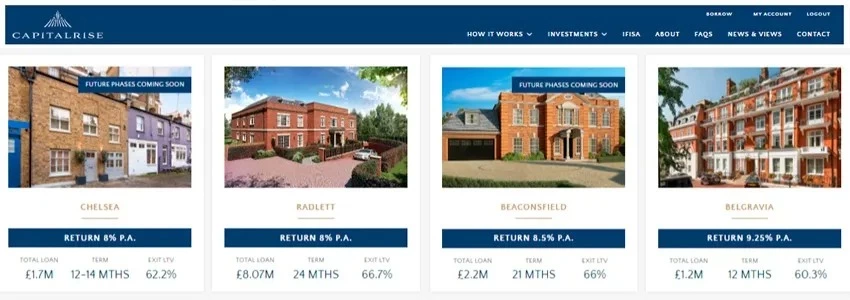

I think the one thing that makes us truly unique is the quality of the real estate that we focus on. The projects we've funded so far have been in locations such as Eaton Square, Grosvenor Square, the Strand, Belgravia and Knightsbridge to name just a few.

With property investments, it’s always about the location. The dynamics of the Prime Central London market are very different from the dynamics across the rest of the UK market and what sets it apart is its resilience.

The property market is cyclical, but if you look back at data from last 50 years (since they started tracking), you can see that at the end of every downturn, Prime Central London bounces back three or four years faster than the wider London market or the UK market overall. Typically, this is because buyers in these locations have a lot of liquid wealth and will always return to the prime central London market because of its worldwide appeal.

CapitalRise is subject to FCA regulations. After Lendy's bankruptcy the Financial Conduct Authority (FCA) has published that it will set stricter conditions to allow investment in p2p lending Platforms. What do you think about these upcoming measures? And do you already have a work plan in place to adapt?

Companies must be regulated to operate in our sector. We are currently an appointed representative of a firm called Sapia Partners, but have applied to the regulator for our own direct authorisation and our application is now being processed by the FCA.

It's quite common for early stage firms to use a third party appointed representative scheme, because it can take a year or more to get your own license. This is a way you can work with a third party to get out and launch your business within a month or two.

We are technically a crowdfunding platform and therefore fall under crowdfunding, not peer to peer lending regulation, which is slightly different. In fact, a number of the new regulations for peer to peer lenders are already in place in the crowdfunding sector.

At CapitalRise, we have had investor categorisation and appropriateness tests in place since inception. From my perspective, the new FCA measures are great and we welcome them because they'll create more of an equal playing field between those of us in the crowdfunding space and those in the peer to peer lending space, bringing them up to a higher level of regulation, which we already fall under.

What prospects do you see for the English property market and how will it be affected by Brexit? And do you have any concerns about the subject, or do you think it could affect your business?

Our core focus is prime central London property, a market which is in a very different place within its cycle from the rest of the UK market. The prime central London market has been in decline since the end of 2014 and is now bottoming out, with house prices down c. 20% versus the peak.

From our perspective, the bottom of the cycle is a fantastic point to be lending and investing. The average loan-to-value (LTV) across our loan book to date is 64%, so that means property prices would have to fall by a further 36% for our investors’ funds to be at risk, bearing in mind values have already come down 20%.

Just to put that into context, the biggest price fall in Prime Central London, since records began was 25.6% in the 89 recession, so we believe a fall of a further 36% at this point would be an unprecedented situation.

We lend against independent, third-party red book valuations and valuers are already pricing in market changes and Brexit uncertainty. Therefore, as a lender, we are comfortable to be lending against what is already quite a conservative valuation at an average LTV of 64%.

CapitalRise has recently closed a funding round, of more than £2.3 million, with Seedrs, with a business valuation of £16m, which I think is impressive, and it also speaks very well of the excellent work you're doing. And recently you have secured a £30m institutional funding line. Can you tell us CapitalRise’s plans for next year?

The plan for us is to continue scaling the business in a controlled fashion, whilst maintaining high quality underwriting standards. I'm very proud of our track record with no losses and defaults to date and I want to maintain that.

The funding line will be used to fund larger loans. One of the ways in which we will scale is by underwriting larger ticket loans and we know there is market demand for this. Some of the loan applications we see are for £50 million plus, so these institutional funding lines will help us to fund larger loans that we couldn't currently fund quickly via our members.

To conclude, could you please tell us what are the main values of CapitalRise and what makes you different?

The number one thing for us is quality: the quality of the real estate and the quality of the team sourcing and underwriting these opportunities. I think that quality is probably the main differentiator for us when compared with other platforms.

I would urge anyone thinking about investing with us to do their own due diligence on us as a team, on the opportunities we offer, our previous transactions and track record to see whether they agree, but for me, quality really is the most important value that underpinning everything we do.