Interview with Roxana Mohammadian-Molina, CSO at Blend Network

"We are not interested in being the largest platform in the UK or Europe, but we are interested in being the best platform in terms of quality and having zero defaults."

Roxana Mohammadian-Molina holds an MSc in Financial Economics and Econometrics and a BSc in Quantitative Economics and she is Chief Strategy Officer at Blend Network. She is responsible for the platform’s growth and strategic partnership alliances and today we discussed with her about their approach to peer-to-peer lending and their focus on property-secured loans:

Tell us about your background and about your own experience as an entrepreneur.

I have a financial background and worked for many years in London, in Investment Banking, at Barclays and at Morgan Stanley. Mainly I was involved in investment and trading in oil and commodities.

In 2015 I quit banking because I wanted to undertake my own project and I set up an online BeautyTech platform called Zeebba which was dubbed the ‘Uber of Beauty’. If for example a person was at home, in the office or a hotel and wanted for example a hairdresser or someone to do the manicure, with our App was able to select the service and the professional would move to the client's home. And the truth is that it went really well and after eighteen months I sold the company to a big American company, called Urban Massage, which already offered massages but wanted to expand into the beauty sector.

Blend Network was started by Yann Murciano, a former colleague of mine at Morgan Stanley. Yann Murciano was the head of metals trading at Morgan Stanley and in 2016 he left banking to launch Blend Network. I then joined him in 2017. When I worked in banking, I had always invested in real estate and knew the sector, so when Yann offered me to join him it seemed like a super interesting opportunity because there was clearly a niche in the market to connect investors with developers looking for funding.

You have been recently listed on Innovate Finance's Women in Fintech Powerlist. What is your experience as a woman entrepreneur?

Obviously, there were very few women working in banking when I worked there and then I thought that in the Fintech world there could be more women because it's a more creative sector, but the truth is that we're still a minority. On top of that, the statistics also show that it is much harder for women to raise investment, especially from Venture Capital (VC).

I personally haven't had these problems because of my experience in the investment banking sector, which is a very aggressive world and prepares you very well to face the challenges of raising capital.

Thankfully some platforms are increasingly trying to support women entrepreneurs and are allocating resources and funds to support women-founded projects and companies. But there is still a lot of work to be done as we are still a minority.

Let's go with Blend Network. What is your approach as a peer-to-peer lending platform?

At Blend Network we connect people who need short-term loans to develop real estate projects with investors. On the one hand, in the last ten years after the crisis, interest rates on banks are very low and people who have money are receiving virtually no interest and are looking for opportunities to invest in. And on the other hand, the banks are not lending to small property developers and they are not getting financing. And what we do is connect these two groups.

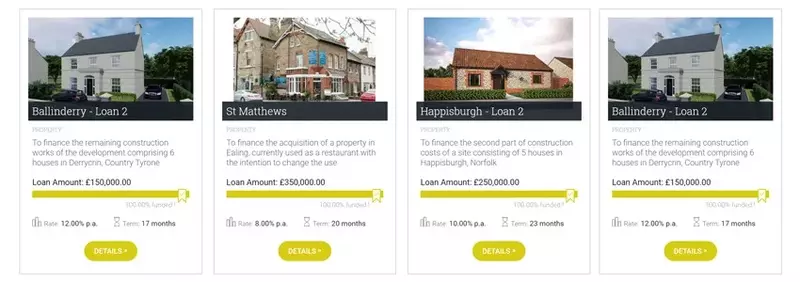

So, at Blend Network we exclusively lend to property developers who are looking to build more affordable housing. We do not lend to any other type of business. The reason is that all our loans are secured against property. And this is something very important, because in this way we always have that property as a security for our loans.

In addition, we always co-invest our own funds in each project and this is an additional guarantee to our investors because it shows them we have ‘skin in the game’. Lenders see that we are not just brokers that connect lenders and borrowers. We actually lend to the projects ourselves.

Do you have any restriction on the maximum amount you can co-invest in each project?

The only restriction that the FCA has placed on both us and our lenders is that in total no more than 10% of investor’s net worth can be invested in peer-to-per lending.

In order to invest in our platform, when prospective lenders register, they must answer a 5-question test to demonstrate that they understand the risks inherent in investing in peer-to-peer lending. And one of those questions we ask is precisely whether the investor is going to invest more than 10% of their net worth. And if they answer yes, they could not register on our platform.

This investor appropriateness test is now going to be mandatory with the new rules that FCA is going to introduce, but that’s something that we have already been doing from the very beginning.

Why did you choose the name Blend Network?

It's very easy. We're in business lending, so the Blend part of the name comes from combining those two words: Business Lending. And the Network part is because our investor network that is also a fundamental part of our approach. So, our name defines what we do: a network of investors in business lending.

And that's why do you define yourselves as a 'Lending Club' instead of a more traditional 'Lending Platform'?

It's a question of closeness or belonging. People like to be in a network of investors, but above all they like to feel that they are inside and that they are part of a club. When you register in Blend Network you receive a series of exclusive notifications about our investment opportunities and you become part of our select Lending Club.

You are based in London, but you lend all across the UK but outside London. Why?

Because we are focused on lending to experienced yet small and medium property developers who build more affordable houses with a value between £200,000 and £300,000 on average. The UK has a huge shortage of such affordable housing and that's precisely the niche we're focusing on. We are lenders and what we want is our borrowers to pay us back in a maximum of 24 months.

We don’t tend to fund ‘white elephants’ meaning that we don’t fund expensive houses in prime locations because we believe that the UK market does not need those properties and the UK is making those properties hard to sell. In other words, the exit is very difficult for high-end properties in prime locations in the UK. However, the market for the more affordable houses that we focus on is a very liquid market. Indeed, our borrowers are selling off-plan which is unheard of in London right now. That is our niche and our strentgh.

And what kind of investors do you focus on?

Generally, I would say we have two types of investors. On the one hand, we have high net worth individuals and family offices who can lend north of £50,000 on each loan.

And on the other hand, we have private investors who can lend any amount from a minimum of £1,000. What these private lenders like about our platform is that it allows them to access the exact same investment opportunities as large sophisticated investors and with same conditions. This is important because private investors with a few thousand pounds to invest are not be able to invest in a hedge fund or some other sophisticated financial product, but peer-to-peer is democratizing investments by giving them access to the exact same deals as large and sophisticated investors.

What fees do you charge to both lenders and borrowers? What is your business model?

Investors do not pay any fee; what they see is what they get. We only charge property developers who are the ones borrowing the money. The interest rate is around 1% per month and we charge them an upfront fee of around 3% to do the due diligence on the project.

And are you also authorized to offer IFISA?

No, not at the moment. It may be an option for next year, but at the moment we are not authorized to offer them.

Could you give us some overall figures on Blend Network? Average profitability you are offering, number of investors, average ticket, etc.

Our average return so far is 11.3% p.a. and we have 0 default. I think we have one of the highest average returns in the sector in the UK and that is precisely because of our niche approach. For example, last year we did 80% of our lending in Northern Ireland, which is a very strong market but there are not many lenders there.

Lenders can lend any amount from a minimum of £1,000. The average ticket for our investors is around £8,000. Although, as I mentioned before, we have lenders who lend £1000 and others who lend £100,000 on each project.

The average time it takes for a project to be funded is only a few minutes. At first it took several days, but now it only takes a few minutes. In fact, we have had projects that have been funded exclusively with 'Auto-lend'.

We have funded 31 projects since we launched in January 2018.

And in terms of the number of investors right now we have north of 1,300 registered investors.

How is the investment process at BLEND Network?

The registration process is very simple. You only have to go to our website, register and provide us with a proof of ID so that we can carry out AML and KYC, which we do in 24 hours.

We accept investors from all countries except the United States and, of course, we do not accept investors from countries identified by the European Union as suspected of money laundering or terrorism financing.

And to invest it is not necessary to provide us with a bank account, simply once registered the investor must transfer funds to their e-wallet to invest in the project they want. And in the same e-wallet will be deposited interest payments, which may then be reinvested in the platform or transferred to their personal account.

BLEND Network raised £10 million of a late-seed financing round last year. Can you tell us a little more about how the process was to capture that amount and how your growth plans are going?

We decided not to use any crowdfunding equity platform, nor any private equity firm, as these types of companies put a lot of pressure on escaling and increasing your metrics at any cost, so that you become the next unicorn. And for us, from the beginning, our focus has been on the quality of our loans. We are not interested in being the largest platform in the UK or Europe, but we are interested in being the best platform in terms of quality and having zero defaults.

That's why we decided to rely exclusively on our own network of private investors, who share our values. They understand that quality is more important than quantity and that we are not going to issue loans just for the sake of growing our loan book, but that we are going to be very exclusive and that we are going to focus on having very good quality loans. And, in fact, most of the investors who entered the round were already users of Blend Network, who invested in our loans and seeing the work we do, have been encouraged to invest in the company as well.

And the money is being used mainly to grow the origination part of loans. Our focus is on attracting more projects and this year we've hired three senior people, whose job it is to get more good quality projects. And the challenge is to get that balance between investors and projects, producing a good return and keeping zero defaults.

To conclude, what would you say are the greatest values of Blend Network and why should investors choose your platform to invest in?

We are a small company and we have always been clear that our goal is not to be the biggest. Our ambition is to be the best in terms of quality and our focus is therefore on the quality of loans and on staying in our niche market.

It is also important to note that we always invest our own money in each of the loans we offer to show ‘skin in the game’.

We also are a member of Innovate Finance the association that represents Fintech companies in the UK.

Recently in an article we were defined as the Goldman Sachs of peer-to-peer lending and we are very proud of that. We put a lot of emphasis on due diligence on each of the loans.

In a nutshell, we want to be the best platform in terms of quality, keeping our track record of zero defaults and continue offering a high returns to our investors.