Interview with Oksana Katalkina, CEO of LEORM

"There was a gap for qualitative property-backed real estate development business projects in the Baltics and that's why we founded LEORM: offering our investors to invest in high quality property backed loans."

LEORM is a crowdlending platform focused on qualitative property backed loans in the Baltics.

Today we talk to Oksana Katalkina, founder and CEO of LEORM, a crowdlending platform registered in Estonia and focused on the real estate development projects of the Baltic States.

Oksana, thank you very much for your attention and for talking to us. Before we talk about your company, we would like to get to know you a bit better. You studied finance at the University of Latvia and then you did a Master in Finance and Financial Management Services. Could you tell us more about your personal experience and background before you found LEORM?

I obtained my master’s degree 16 years ago. In 2019, at the same time when the LEORM crowdfunding platform was created, I decided to go on with my studies. Thus, I am a PhD student, and my doctoral theses is associated with some aspects of crowdfunding. Before we had registered our operator of the LEORM crowdfunding platform in Estonia (LEORM, OÜ), in 2019, my personal expertise was finance management. My professional background includes financial analytics, M&A, development and evaluation of investment projects.

And 2 years ago you decided to found LEORM together with Otomars Ushatskis. Can you tell us how you met and how the idea of founding LEORM came about?

I knew LEORM’s co-founder Otomars Ushatskis a long time before we made LEORM. Otomars is an experienced real estate trader and analyst with excellent real estate market sense. Before we decided to make the crowdfunding platform, we were developing one real estate project where we were trying to attract an institutional investor. The project was worth investing in, but the project’s originator did not have sufficient track records.

Thus, the idea of creating a crowdfunding platform came itself, since it was a logical sequel for the application of our skills in rendering a full spectre of services for SMEs’ projects.

Before this, we succeed in so-called “club” and institutional financing attracting for projects (in total, for 64 projects). This track record is mirrored on our platform since we wanted to stress out our previous experience in this matter.

There are already many Crowdfunding platforms, why did you decide to launch a new platform? And why did you focus on the real estate sector?

We investigated the market and we knew that the competition in the crowdfunding market is rather severe. Meanwhile, we saw the gap for our crowdfunding activity in providing qualitative investment product, namely, to offer investment opportunities in loans for qualitative property-backed real estate development business projects, since we were advisors and facilitators in institutional and private equity financing attracting for such kind of projects. The focus on real estate was made after the rigorous study of the Baltic market’s situation and analysing of its trends.

What is LEORM and what is its value proposition?

LEORM is a crowdfunding platform for investments in property-backed loans for European business projects. Due to the fact, that we are launching a new category of projects, namely, buy-to-let, we could say that we will cover both crowdlending and crowd investing models.

It should be noted, that we had some other (not real estate) projects, as well, where we financed the acquisition of fixed assets for a company with its activity in the construction industry. We plan to develop this direction of financing, providing investment opportunities in business loans for our investors. Although this type of project is not directly related to real estate, the deals are secured with collateral, without fail.

Your area of operation, for the time being, is in Latvia but you have nevertheless registered in Estonia. Why are you not registered in Latvia and why did you apply for a license in Estonia?

Our area of operation is both Latvia and Estonia. Here, we should make a little excurse in crowdfunding licensing issue in the Baltic States since the issue of the national conflicting framework is rather crucial when choosing a jurisdiction for crowdfunding activity. The Baltic region (Latvia, Lithuania, and Estonia) is not very big, but the licensing matters differ significantly across the countries.

The issue of crowdfunding service providers for business is unregulated in Latvia. Therefore, to avoid the uncertainty of the unregulated market, crowdfunding business financing models choose Estonia as its registration country, even though they are organised by owners and managers of Latvian origin. In Estonia, the market of crowdfunding service provision is partly regulated (in the sense, that Lithuania, for example, has crowdfunding law), namely, an authorisation by the Estonian Financial Intelligence Unit (FIU) is required. One can argue that there are a lot of platforms registered in Latvia, and some of them are the biggest in continental Europe. Yes, it is, but their business model assumes “loan originating”. That means that they collect funds from the public to grant them to credit intermediaries (the companies with consumer crediting license). This is completely another crowdfunding business model, where the end-point of the financing scheme (companies that issue credits) is regulated, that is why this crowdfunding business model is allowed by default, in Latvia.

Therefore, we have obtained a license for acting as a financial institution from Estonian FIU (link to the license: https://mtr.mkm.ee/taotluse_tulemus/517647. ), to act in the regulated market to finance business. With the license, we can address both Estonian and Latvian projects, as well as projects in other countries without specific crowdfunding law. Before we chose the jurisdiction where to register our business, we had studied the issue of licensing from the point of view of our expected business model, namely, what we are going to finance and how.

Continuing with the licence, you are currently registered as a Financial Institution with a licence issued by the Estonian Police and Border Guard Board. How does this affect you and what are your plans for the upcoming crowdfunding regulation in Europe? Do you plan to apply for a licence as an ECSP (European Crowdfunding Service Providers for Business)?

The regulation you are talking about came in force last year, October, and it should be adapted at the Member States’ level this year, November. Crowdfunding platforms will have one year transition period to be authorised under the regulation. Therefore, we do plan to prepare ourselves for the Regulation requirements and to obtain the license, since this is about the trust of investors every crowdfunding service provider fights for. (This is not a secret, the issue of trust is especially vital for any newcomer in the industry.) Moreover, for the time being, the LEORM platform adheres to the principle of best practice for crowdfunding. Meanwhile, one of the regulation’s aim is to foster cross-border financing. Thus, the authorisation under the regulation could be a good tool to address projects in other European Union countries, providing high-level diversification’s opportunities by countries for our investors.

Let us now focus on the operation of the platform. How do you select the projects you offer to your investors? Of all the loan applications you receive, what percentage do you accept?

The main principle we adhere to the selection of the projects for placing on our platform is that they are in growing sectors of the economy (or with potential growth). We conduct a thorough legal and financial due diligence check before onboarding. The entire project study process is performed by at least 3 experts: a financial analyst, a business analyst, and an outsourced expert of the relevant economic sector. Thus, the project study is based on the 6C model applied by different banks, which includes studies of Character, Capacity, Cash, Collateral, Conditions, Control.

The use of the method can ensure an adequate way to estimate a borrower's ability to repay a loan, as it includes qualitative factors, not only quantitative. Our statistics of accepting the projects shows that approximately 60 per cent of the projects are ejected. Meanwhile, sometimes this is our initiative to offer projects’ originators to be listed on our platform with their projects. Before we offer our services, we collect information about the projects’ originators and their projects. Our everyday work includes this activity. We make efforts to know each project’s originator personally, as well as it's business. We think that the remote automatic approach is not the right one when dealing with investors’ funds.

What kind of guarantees do you offer investors?

The main rule for us is to assess collateral, evaluate a project and a project’s originator (both company and its owner/s) itself. That means that we conduct a multi-step process before deciding on accepting a project. What we want to achieve with the process, is that we accept only the projects where we are sure our investors will get their invested money back.

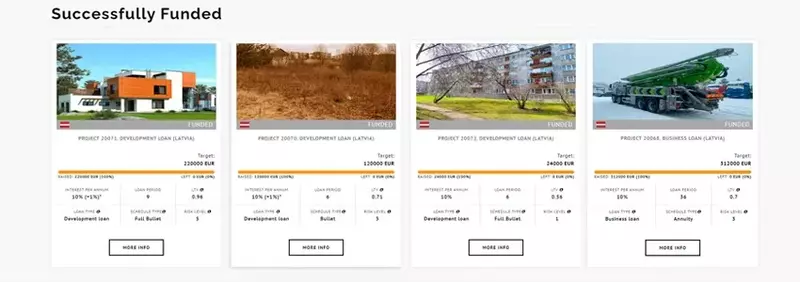

To date you have funded 8 projects on the platform. Have you had any delays or default in the payment of instalments? What is your track record?

No, we had not had any delays both for crowdfunded projects and for “club” financed projects. Our projects’ selection criteria is rather high, and we want it to be the same in the future. Meanwhile, investors should always keep in mind, that past performance is not a guarantee for future returns, and not only in crowdfunding.

Does LEORM participate in the development or management of the projects it offers?

Yes, sometimes we do. We participated in the development of some projects, but always with a separate company, which is fully segregated from LEORM and investors’ funds. Meanwhile, the legal procedure when dealing with this separate company always is the same as with other projects’ originators. The company provides collateral that is legally registered in property registers of the states of the projects.

How do you see the real estate market in the Baltic States and what is your forecast for the coming years?

We consider that making the forecasts for upcoming years, one can put itself in a very unfortunate position. We just analyse common trends and effective demand for real estate in the Baltic market.

The main trend remains that the Baltic States have a relatively underdeveloped rental market. Apartments in a good condition and for a reasonable price are rented out in a couple of hours, and there is a great shortage of this type of property in the market. Meanwhile, banks are increasing requirements for lending conditions. Therefore, this moment is the best one to buy-to-let or develop residential and commercial buildings by financing the deals via crowdfunding.

Moreover, the structure of the real estate demand has changed significantly due to the quarantine situation in the countries, namely, a lot of people prefer selling their city apartment and buying small but energy-efficient suburb houses. At LEORM platform, we provide mostly such kind of projects, since we make an accent on collaboration with mid-class suburb residential villages’ developers.

If we analyze the current trends of crowdfunding real estate financing, in our opinion, this could become the main means for financing real estate development projects, and not only for emerging markets' projects. Perhaps, the outline will be transformed, since we still do not know the future of fiat money, but the main principle will remain.

What are LEORM’s plans for next year and where do you think you'll be in five years?

We have our strategic plans concerning the Baltic assets, mostly. As for the mid-term future planning, I think, it very much depends on the financing conjuncture on the whole.

That's not a secret, that the cause of this rapid growth of business financing through crowdfunding was tightened requirements for financing from banks. On the one hand, that has given a lot of good projects to the crowdfunding investors which cannot be financed via traditional financing due to various reasons. On the other hand, negative deposit rates (in the EU), have forced a lot of investors to take their funds from deposit accounts and invest them in assets and loans via alternative financing instruments (like crowdfunding), to avoid additional money-storage expenses.

The combination of these two factors alongside the expected growth of inflation became the major aspect of the rapid growth of the crowdfunding market. We understand this mechanism very well and think that the situation could change anytime. Meanwhile, we do think about the paradigm shift in business financing in the future. Anyway, we are rather flexible and we invest our time in studying the market to try to foresee and react timely to the changes, especially, from the point of view of tailoring our activity to the needs of our investors.

To conclude, what would you say is the greatest value of LEORM?

We can express it in three words, which we have declared on our platform: Safety, Profitability, Stability. To summarize, on the LEORM crowdfunding platform investors could expect investment opportunities in high-quality business projects loans backed by property and buy-to-let property deals.