Interview with Bert Reila, Affiliate Marketing Manager at EstateGuru

" EstateGuru is the leading European marketplace for short term property lending and our main goal for the next years is to keep growing, increasing the loan volumes and the amount of investors that we have."

Today we talk with Bert Reila, Affiliate Marketing Manager at EstateGuru, the Estonian platform focused on short term property backed loans:

What's the value proposition of EstateGuru and what sector are you targeting?

First of all, thank you for the interview. If I were to explain EstateGuru in simple terms, I would say that EstateGuru is the leading European marketplace for short term property lending. And what we do is we connect two sides: we connect borrowers and investors.

For our borrowers, our mission is to offer flexible financing solutions. And for investors we offer geographically diversified investment opportunities. Currently there's more than 30 000 investors at EstateGuru and the funded amount is now over 145 million. We have quite a track record already and we are quite big in European terms. And what makes us a bit different from other platforms is that we have investors from all kinds of specialties and walks of life, because our minimum investment amount is just 50 euros, so everyone can join in! And we mostly focus on the European market.

How is the investment process at EstateGuru and how do you structure those investments?

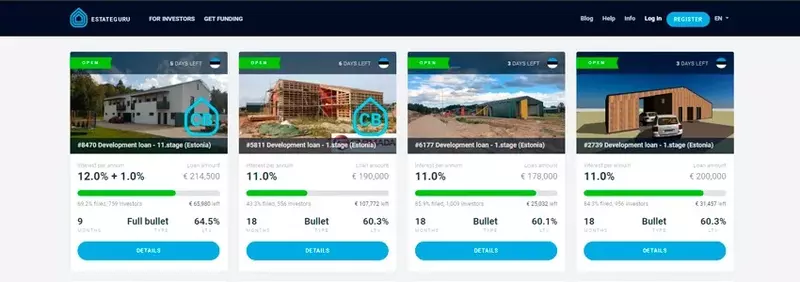

Starting to invest is really simple. You just go to EstateGuru website, you sign up an account and you transfer funds to that account and then you make an investment. Investments can be made by either signing up with a password or a SMS verification code. We have also the auto-invest tool, which makes all your investments passive, automatically for you. So, all you need to do is just transfer funds to that account, so that the auto-invest can work and it diversifies your investments across all loans. Of course, you can set the criteria as well.

And regarding the structure of the investments, when an investor makes an investment into one of the loans at EstateGuru, they get a loan contract between them and the borrower, so the borrower is obliged to return their investments to them. And we have the first or second rank mortgage on the project. So that means if the borrower is not able to pay it back, then we just sell the collateral, so our investors are protected in that way.

Sometimes we do accept second rank as well, but it's something it’s not common, about 5% of projects. And this is solely in cases where already a first rank has been established.

And I will also point out that in Estonia, and also in the countries we operate, the first rank mortgage is something that nothing can overcome. So, for example, if another party has established a second rank mortgage on the project then we would have the first rights to any funds received from the sales of the collateral.

Could you explain me a little bit more about this loan agreement?

How the loan agreement works is that when an investor enters a loan contract, they are the lender and they enter into the contract directly with the borrower. So, the lender, which is the investor, agrees to lend a sum of money to the borrower and the borrower is then obliged to pay back this same sum to the investor plus interest. And it's a direct deal between the borrower and the investor. And EstateGuru is only the representative of investors in any loan issues, so EstateGuru acts in the best interest of the investors and has to ensure that the loan is paid back according to schedule.

And how does EstateGuru handle the funds?

I would like to point out that investor funds are handled separately from all of the firm funds. They are held at the LHV Bank of Estonia on a separate account. So EstateGuru does not influence the funds of investors in any way. So, all of the funds from all investors are pulled into that one account, which is for holding the investor funds.

Does EstateGuru participate in the development of the project or do you co-invest?

No, EstateGuru does not co-invest in the projects we offer. Nor do we participate in the development of the projects. As I said before, we just intermediate between the lenders and the borrowers.

What's the business model for Estate Guru? What commission do you charge to investors and to borrowers?

From investors we do not charge anything, investing is absolutely free. But from the borrowers we charge a 3% success fee and also an annual administration fee, ranging between 0% and 2%, to administrate the loan. So, this makes up the bulk of our income.

EstateGuru is not regulated by the EFSA (Estonian Financial Supervision Authority), because according to the Estonian law, you don't need a license to intermediate in business loans. Then, does EstateGuru have to comply with any regulations or is it audited or supervised in any way?

As EstateGuru only intermediates in business loans, and the platform is registered in Estonia and operates in Estonia, then no license is required. Currently we are officially operating only in Estonia and Latvia, and both countries need no license for crowdfunding. And in other countries our operation is carried out following the principle of reverse solicitation.

And about upcoming regulation, we are currently one of the leading forces in a task group that was created in Estonia by the Financial Inspection to create some laws for crowdfunding, and EstateGuru was included in that group. And the first regulations can be expected maybe at the end of this year or maybe at the start of the next one.

And we are also members of Finance Estonia, which is not an official regulatory body, but all of us who are members are committed to following best practices and to accept their supervision.

And do you offer any other type of guarantee to protect investors, such as a buyback guarantee?

No, we don't have a buyback guarantee because all the platform loans at EstateGuru are already secured by a mortgage and that's the guarantee that investors get when they invest.

And how it works is that, let's say there's a project of €120,000 and let's say the collateral value is €300,000 and that we have established the first rank mortgage on the collateral real estate, that the borrower has agreed when they signed the loan contract. So if the borrower does not pay back the funds that they owe to the investors, then we just put his house, or whatever collateral real estate (land, apartments) they have, up for a public auction. And when the public auction is successful, then the funds are given back to investors.

Could you give us some overall figures on EstateGuru?

The number of projects that have been funded is more than 980 and the amount funded to date is more than 145 million euros. The average annual yield for investors at the moment is 12,1%.

And what about your track record?

Our default rate is 3% from the whole portfolio. This is something that we deal with every day. We have a specialized debt management department inside our headquarters. And their task is to everyday ensure that, with that projects that have defaulted, they recover those funds and enforce the real estate collateral.

And of all the loan applications you receive, what percentage do you accept?

For the due diligence process, each loan project has a separate mortgage placed on it. We have robust credit policy which is mandatory to be followed in analyzing every project. In general, our credit analysis consists of two parts – analysis of the borrower and real estate assessment. Besides the background of the borrower, we also analyze the financial statements (credit scoring). As a rule, we use only real estate valuations from independent evaluators and critically review them by ourselves. If the projects are complicated our lawyers also do full legal due diligence. After the loan managers have prepared the loan documentation with the cooperation of the risk department all projects will be sent to EstateGuru’s credit committee for final approval. The credit committee is based in Estonia and consists only members of the risk team (independent from the sales side). The committee is the highest credit decision-making authority in Estateguru and it follows and implements the group's credit policy. The creditworthiness of a borrower is determined by an assessment of financial reports and collaterals, repayment ability and capacity, borrower’s credit score and payment remarks with credit history. Also, the background of the personal suretyship giver is analyzed. Committee also decides which collection actions should be taken on late and defaulted loans. The credit committee will make a decision (approved, rejected) and if necessary will ask additional information from the loan managers. As a rule, all of the members of the credit committee have to agree for the decision to be approved (unanimous decision).'So currently only about 50% of the loan applications get approved. But, since the rules and regulations are going tougher in all over the EU, than we see that the amount of applications that get accepted has been decreasing.

Do you accept foreign investors?

Yes, EstateGuru accepts foreign investors as long as they have a bank account in the European economic area or Switzerland.

What are EstateGuru’s plans for next year and where do you think you'll be in five years?

For the next year we're going to stay focused on growth and also on expansion in Europe. So our main goal is to increase the loan volumes, get more projects launched in the platform and also to increase the amount of investors that we have.

But at the same time, we want to create more cooperation with other Fintechs, Proptechs, and also traditional financial institutions. So for example, just a few weeks ago we started cooperating with the LHV Bank of Estonia, so now all the LHV customers that are also investors at EstateGuru can connect directly to their EstateGuru account from their LHV Bank account and check the status of their loans, view their statistics and see how much money they have invested in the platform. And I think this is a good example of cooperation between a traditional bank and Fintech.

We are also closely monitoring the regulation situation and, as I said before, we want to be the leading force in creating this regulation as we are firmly committed to this new regulation as we believe that it will be very beneficial to both parties, both our investors and ourselves.

To conclude, what would you say that is the greatest value on EstateGuru and why investors should choose your platform to invest in?

it's hard to pinpoint a certain value, so I'm going to bring out five:

✔️ The first thing is that all of the projects that we pick are picked by our professional real estate background risk team after a thorough due diligence process.

✔️ Secondly, all the investors at EstateGuru can see their investments in real time, they can track their progress and they can pick the projects themselves as well. They have a lot of information about each project, so they can base their investment decisions on that.

✔️ Thirdly, the minimum investment sum is just 50 euros. So even if you don't have a big amount of funds available, you can start investing easily. And there are no hidden fees, so investing is free.

✔️ Fourthly I have to bring out that the average yield is 12.1%, which is larger than a lot of other crowdfunding platforms and also larger than traditional investment opportunities.

✔️ And for the last thing, all of the projects are backed with a mortgage. So if the borrower is to default, we can still recover the funds of the investors as we always have a collateral.